SMM July 9 - SS futures held up well today. Spot market, the overall market remained basically stable.Affected by yesterday's low-price transactions of high-grade NPI, retail quotations fluctuated, market sentiment was somewhat impacted, and low-priced supplies increased, while transactions remained mediocre as before. Currently,stainless steel mills have basically completed the distribution of July contract volumes, easing their pressure. However, social inventory remained at a relatively high level, downstream demand was difficult to improve significantly during the current off-season,and traders still faced considerable sales pressure.

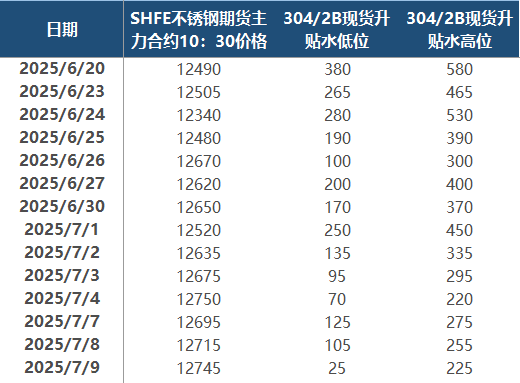

Futures side, the most-traded contract 2508 held up well. At 10:30 am, SS2508 was quoted at 12,745 yuan/mt, up 30 yuan/mt from the previous trading day. In Wuxi, spot premiums/discounts for 304/2B ranged between 25-225 yuan/mt. In the spot market, cold-rolled 201/2B coils in Wuxi and Foshan were both quoted at 7,500 yuan/mt; cold-rolled edge-trimmed 304/2B coils averaged 12,700 yuan/mt in both cities; cold-rolled 316L/2B coils in Wuxi were priced at 23,600 yuan/mt, same as Foshan; hot-rolled 316L/NO.1 coils were quoted at 22,900 yuan/mt in both locations; cold-rolled 430/2B coils in Wuxi and Foshan both stood at 7,100 yuan/mt.

Currently, the stainless steel market remains in the traditional off-season,with downstream demand failing to match current supply levels. Additionally,uncertainties such as US tariffs still loom large, leading to strong wait-and-see sentiment downstream. Although stainless steel mills generally face losses, and production cut news has emerged, the massive production base from earlier periods keeps current market supply at historically high levels,meaning supply-demand relationship recovery will take time. Both mill inventories and social inventories remain at relatively high levels, with destocking slowing significantly during the off-season, puttingstainless steel mills, agents and traders under heavy sales pressure, thus limiting price rebounds. Raw material side also faces immense pressure. Affected by expectations for production cuts at steel mills, only high-carbon ferrochrome prices remained stable in steel tenders due to overseas ferrochrome producers' output cuts, but retail prices already fell below tender levels. Other materials likehigh-grade NPI and stainless steel scrap prices also weakened noticeably, further eroding cost support for stainless steel. The market is waiting to see how the supply-demand relationship will recover after stainless steel mills cut production.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)